As you’re attempting to improve your credit score—particularly when you’ve quite recently begun your organization and are attempting to construct new credit—activities like paying on schedule, and blending the sorts of credit you use, will all help your business financial record and accordingly, business credit score assessment. But then again, activities, for example, missed payments, balances exceptional, and current decisions would all be able to bring down your credit score assessment.

In the event that you’ve at any point been available for a purchaser credit, for example, a home loan, you presumably have an idea about your individual budgets. You know where your own credit score assessment stands month-to-month and what individual credit means for your capacity to fit the bill for monetary items. Yet, as an entrepreneur, you probably won’t know even a little bit about your organization’s business credit score assessment—why this is significant, what your rating is, or how to set up and fabricate business credit.

In the event that you’ll, at any point, need to improve your credit score later on—with a small business loan or business credit card, for instance—your business can’t simply get by with a solid individual credit score rating, you’ll have to construct a positive business record of loan repayment.

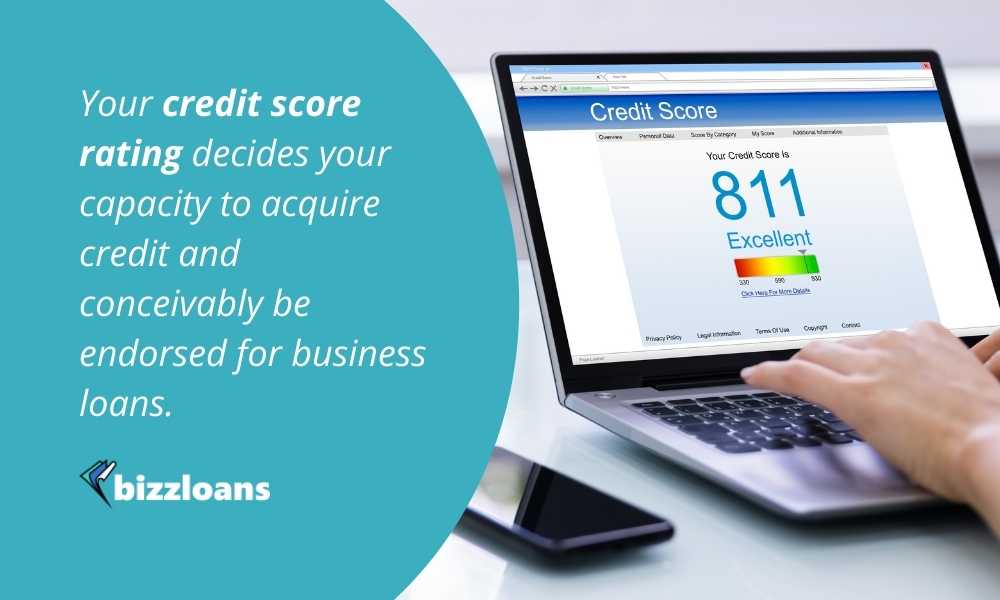

The data on your credit report straightforwardly impacts improving your credit score. Your credit score rating thus decides your capacity to acquire credit and conceivably be endorsed for business loans. Having a helpless credit score rating will either hold you back from acquiring credit out or place you in a high-hazard classification, which implies that assuming you’re supported for credit or loan, the loan fees you’ll be offered will be altogether higher than somebody with brilliant credit. Over the existence of a home loan, home value credit, vehicle loan, or understudy loan, for instance, this can cost you a huge number of dollars in revenue expenses.

Now, you ought to have a vision of how business credit functions. Right off the bat in the existence of your company, you’ll need to zero in on your time and consideration in improving your business credit score. Despite the fact that it requires some investment to get business credit, by assuming responsibility for your business’ record as a consumer, you’ll begin to comprehend it more and perceive how various activities influence your credit score assessment.

Improving your credit score, however, is most certainly something you can do yourself. Here are some dependable techniques you can utilize. Each of the accompanying 10 stages can affect how to improve credit score as a consumer, and ideally, to improve things:

1. Have your Credit Score Balance Low

To improve your credit score, the way that you handle credit cards can impact your credit score assessment. Your payment history on your Visa accounts likewise impacts your score. A figure that is viewed as the computation of your credit score rating is your credit card adjustments; having a balance that addresses 35% or a greater amount of your generally speaking accessible credit limit on each card will really hurt you, regardless of whether or not you make every one of your payments on schedule. Assuming you have a $1,000 credit limit on a charge card, in a perfect world, you need to keep a total of under $350, and make convenient regularly scheduled payments on the balance that are over the necessary month-to-month essentials.

To illustrate, let’s take your financial records as an example. Let’s say that you’re effectively decreasing your balance, while appropriately and capably using your Credit Cards. Contingent upon your own circumstance, it could appear to be easier to spread your Visa obligation north of three, four, or five cards, while keeping your equilibrium on every one of them underneath that 35% of the all out credit limit mark, instead of maximizing one credit card. Assuming you do this, make convenient payments on each card and keep them all on favorable terms. Dealing with your Credit Card obligations suitably won’t just hold your Business Credit score back from dropping, it could likewise give it a lift.

Choosing to spread your credit card obligation among a few cards may help your credit score assessment, notwithstanding, prior to embracing this system, ascertain the premium you’ll be paying and analyze financing costs between cards. Sometimes, you might set aside cash by solidifying your Visa adjusts onto one low-premium card, instead of having that equivalent balance spread north of a few higher premium bearing cards. Figure out what works better for you, in order to assist yourself in making the proper choice and making that move that can easily help your business credit score in the long run.

2. Have good Credit Score History by maximizing past credits

In improving your credit score, one of the elements to think about while ascertaining your financial assessment is the time allotment you’ve set up for every creditor that you currently have. You’re compensated for having a positive, long haul history with every creditor, regardless of whether the record is latent or not utilized. The more extended your positive record as a consumer is with every creditor, the better.

Knowing this, try not to close more established and unused records. In the event that you have a small bunch of credit cards you never use, rather than shutting the records, basically put the charge cards in a protected place and disregard them. In spite of the fact that you would rather not have too many open records, having five or six credit card accounts open, despite the fact that you just really utilize a few cards can be helpful. Moreover, assuming that you have a five-year vehicle loan, for instance, showing three, four or five years of positive payments history (with no late or skipped payments) can be a great deal of help.

3. Open up a Business Bank Account

As we expressed initially, it’s fundamental to improve your credit score, and as a rule, you need or may need to isolate your business and individual budgets. In picking your business element, starting a business ledger is an urgent move to define a boundary among business and individual costs. By opening this record, business credit authorities can without much of a stretch see what cash you’re removing from and placing into your business, and will report that data on your business credit report.

You’ll first need to investigate your choices and open the business financial records that are best for your organization. And when you finally open your record, obviously, it’s essential to fully utilize it. You should utilize this ledger to pay for costs of doing business—everything from utilities and lease to your business phone. These buys, as long as you cover them and on schedule, without fail, you positive and additional numbers when you’re trying to improve your business credit score.

All things considered, starting a business financial balance won’t just give a bank reference to your business’ credit detailing offices, it will likewise open entryways for improving credit score later on—the best private company moneylenders search for borrowers with business ledgers that have been set up for several years.

4. Pay bills on Time

Albeit this methodology might appear to be incredibly self-evident, late payments are the most widely recognized piece of pessimistic data that shows up on people groups’ credit reports and are regularly liable for critical drops in credit score ratings. With regards to loans and Credit Cards, you must consistently make basic payments sooner rather than later every single month, without any exemptions.

The effect on improving your credit score assessment will be impressive when assuming you’re never late on making loan or Credit Card due payments, nonetheless, making late payments on different kinds of loans or defaulting on any loans will deplorably affect your credit score rating that will have a lasting effect on your credit scores, some for as long as seven years even!

The advantage to having credit cards is that you can decide the amount you spend utilizing them, then, at that point, conclude the amount you wish to take care of every month, as long as that sum is equivalent to or more prominent than the base regularly scheduled payments due. This permits you to plan your cash and settle on insightful choices, in view of your monetary circumstance. Just paying the essentials on your credit cards will hold those records back from being late, notwithstanding, the expenses related with that choice (as far as charges and interest) will regularly be huge over the long run. Furthermore, this methodology will keep you from extraordinarily diminishing or taking care of the obligation of improving your credit score.

One of the most noticeably terrible slip-ups you can make, beside making late loan or credit card payments, is having a record become delinquent. This implies that you’ve forgotten to pay your month-to-month essentials or have skipped payments for quite some time and the record gets gone over to an assortment organization. When this occurs, whether or not at last make the payments or settle the record, your financial assessment will be adversely affected.

5. Get a Business Credit Card

As an initial step to improve your credit score, you should seriously think about applying for a business Visa to cover everyday purchases for your business. Utilizing a business credit card will likewise assist with setting the detachment between your own and your business’ funds.

Furthermore, a business credit extension works similarly as a Visa, less the actual card. All things considered, the assets you get will live in your business financial balance and you will be able to pull out cash when needed, but this of course still depends upon the situation. Then you simply repay what you get to reset your equilibrium. The demonstration of getting and reimbursing assets on a business Visa or credit extension will assist with building a business credit score—considering that you’re paying on schedule (or early, if conceivable) and in full.

6. Only Apply for Credit When It’s Needed

One way of improving credit score is assuming you’re on the lookout for a lot of new machines or other expensive things, it’s normal for customers to stroll into a retailer and be offered a markdown and a decent financing bargain on an enormous buy, assuming they open a charge or credit card account with that retailer. Prior to applying for that store’s charge card, read the fine print. Figure out what your loan fee will be and what expenses are related to the card.

Apply for any new credit plan when you totally need it. Rather than applying for a retail location card you will utilize only on one occasion, you could simply utilize a current Visa. Applying for and getting numerous new Visas (counting store credit cards) inside a multi month time span will be unfavorable to your business credit score that you are currently building. Except if you can get a good deal on your buy over the long run and can legitimize tolerating a decrease in your credit scores rating, new credit loans won’t matter for credit you don’t really require.

7. Correct mistakes in Your Credit Reports

One of the quickest and most straightforward approaches to improve your credit score is to painstakingly audit each of your credit reports and correct or update any incorrect or obsolete data that is recorded. In the event that you spot wrong data, you can start a debate and possibly have it remedied or taken out inside 10 to 30 days.

8. Separate Your Accounts later after a Divorce

During a marriage, it’s normal for a couple to get joint charge card records and co-sign for different sorts of credits. Coming into the marriage, the data on every individual’s credit report and their credit score assessment will ultimately affect their companion, particularly when new shared services are opened or a mate’s name is added to existing records. Solidifying every one of your records once wedded makes record-keeping more straightforward. In the event that you do get separated an entirely different arrangement of credit-related difficulties will surface.

Comprehend that when you get a legitimate separation, it doesn’t set one or the two individuals free from their monetary commitments with regards to taking care of a shared service. However long the two names show up on the record, the two players are answerable for it.

As your separation procedures push ahead, make certain to pay off and close all shared services, or have one individual’s name eliminated from each record, which means just a single individual will stay answerable for it.

9. Keep away from Excess Inquiries

Each time you apply for a charge card or any kind of loan, a potential bank will make a request with at least one of the credit revealing organizations. This request data gets added to an amazing report and will normally stay recorded for quite some time. For one year, in any case, the request will somewhat diminish your credit score assessment. Assuming you have various requests in a brief timeframe, this can significantly decrease your financial assessment.

Remember, when looking for a home loan or vehicle loan, it’s allowable to have numerous requests for a similar reason inside a 30-to 45-day time span, without those different requests harming your business credit score rating. In the present circumstance, the different requests will be considered one single request.

10. Try not to Consolidate Balances onto One Credit Card

Except if you can save a fortune in interest charges by combining adjustments onto one credit card, this technique ought to be kept away from. One motivation to keep away from this is that maximizing your Visa will cheapen your credit score assessment, regardless of whether you make on-time payments. Accepting the financing cost computations seem OK, you’re in an ideal situation disseminating your obligation north of a few low-interest Visas. An option is to take care of exorbitant premium credit card adjustments utilizing one more kind of obligation solidification loan or by renegotiating your home loan with a money out choice.

Since we’ve clarified somewhat more with regards to how to improve credit score and how it functions, we should talk about why improving business credit score is so significant. All things considered, assuming you maintain a tiny business, you may be contemplating whether it merits putting resources into business credit by any means—wouldn’t you be able to get by depending on your own credit?

Despite the fact that you actually could get by with simply your own credit, it’s truly not the best practice for entrepreneurs. Besides, as we’ll talk about underneath, there are sure advantages of business credit, particularly great business credit scores. It may not look much, but in the long run, your business, albeit a tiny one, will benefit from a good and improved business credit score.

NEED FUNDING FOR YOUR BUSINESS? GET A FREE QUOTE TODAY AND GET FUNDED!

CLICK HERE TO GET A FREE QUOTE

Share this article